The Q2 2023 Solano County Market Recap

I created this resource for you to share accurate market data & trends we saw in our local area. Below you’ll learn more about last quarter’s shifting market. I’ve included info that’s valuable whether you’re thinking about buying or selling, or you want to be a more informed homeowner in 2023.

# of Homes Sold = 1,078

We started the second quarter with a competitive market that drove up home sales. Then, home sales slowed down with the rise of mortgage rates. Overall, we saw fewer homes sell than in Q2 2022 in our local area.

Average Home Value = $339 per sqft

This is the average in our area to close out the second quarter for ALL homes. If you're a homeowner, I recommend we closely examine how the market impacted your home's value. Let me know if you'd like a complimentary value estimation for your home!

1-YR Value Change =

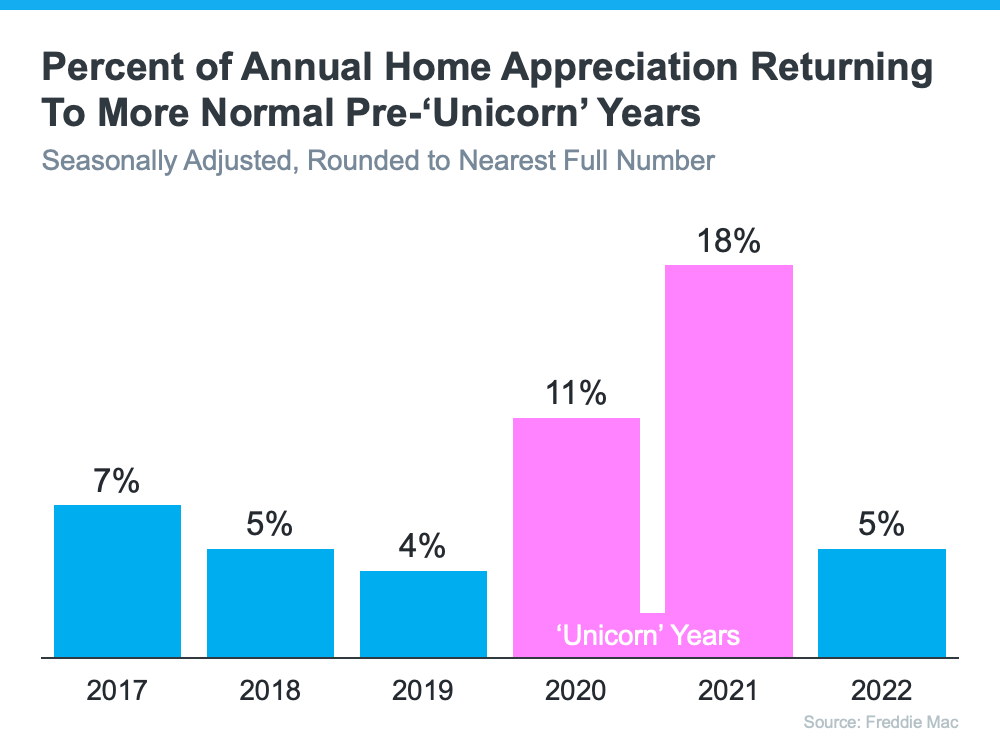

Overall home values are down over last year. In fact, we're seeing an decrease of 7.9%. To put that into perspective, for the past 30 years, we've seen an average appreciation rate of about +4%.

Average Sales Price = $608K

This is the average price a listing in our area sold for. This price is down over last year. If you've been thinking about buying, know that you can benefit from less competition from other buyers in today's market.

Days on Market = 36 Days

This is how long a home is actively for sale on the market before it's pending or goes under contract. While homes aren't selling as quickly as they were in the recent past, our Days on Market stat for Q2 2022 puts this timeframe into perspective.

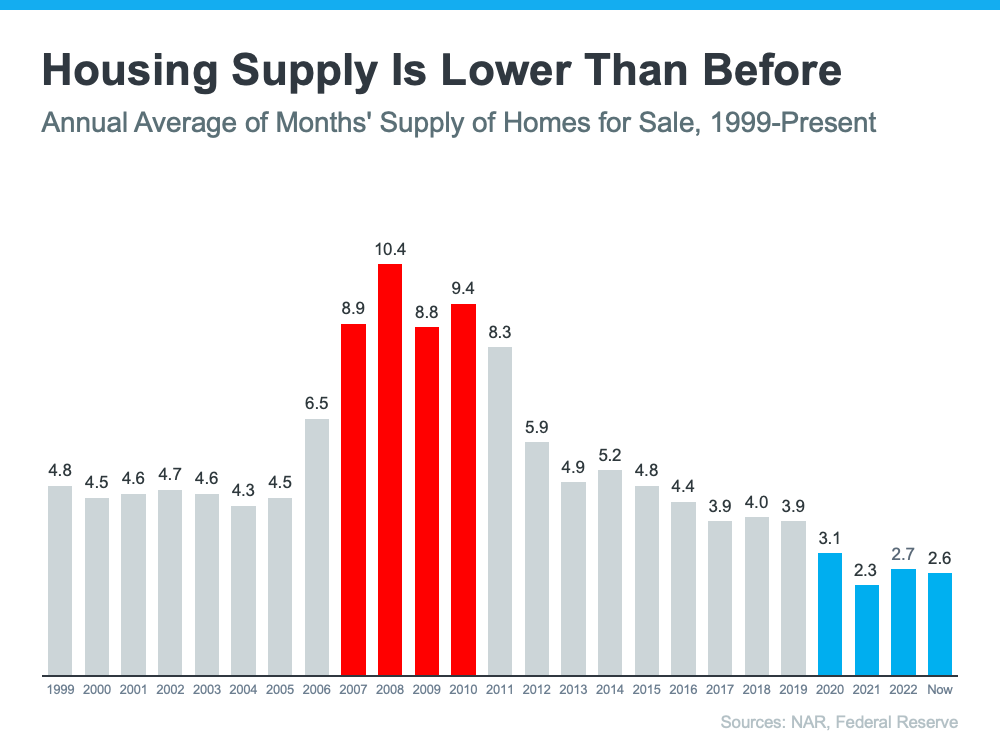

Total Active Listings = 422 homes

At the time this report was created, we currently have 422 of homes for sale in Solano County. To see a list of current inventory - valuable info for both buyers & sellers - please let me know!"

And if you'd like my signature "Real Estate Market Recap" for a different area, please reply back and let me know where!

Note: the market data I'm sharing includes -Data Source: BAREIS MLS. Timeframe: Quarter 2 (April to June 2023). Housing Type: Residential Homes in Solano County. Click here to see the graphs for this quarter’s report.

Thank you!

Thank you for joining me this quarter! As we gear up for the next season, I look forward to bringing you even more tips, trends, and local insights in my email newsletter (subscribe here to get on the list). And as always, if you or someone you know has a real estate need or question, I am always here to help!

Michelle Perez

REALTOR®

Michelle Perez & Associates, RE/MAX Gold

Phone: 707-208-2557

Email: michelleperez@sellwithmichelle.com

Website: sellwithmichelle.com